Shock Value

An oil supply crisis has sparked a repricing of rate expectations among major global central banks. But will central banks respond to a supply shock with rate hikes? Below, we express skepticism about market pricing.

(Published March 20, 2026)

--

Suddenly, there might be value opportunities in global bond markets.

On the eve of the Iran War at the end of February, the bond market expected more than two Fed rate cuts by the end of 2026 but has now flipped to implying a 10% chance of a hike by year's end.

And it’s not just the Fed that has been repriced. Across most major global bond markets, investors shifted from pricing in rate cuts to pricing in rate hikes over the last two weeks (see Figure 1). Notably, markets expected two rate cuts in the U.K. just two weeks ago; investors now see three rate hikes by the year-end of 2026!

Market Expectation Of Total Policy Rate Change In 2026

*Rate cuts and hikes are measured as 25 basis points changes in policy rates

**The Reserve Bank of Australia already hiked rates two times this year

Is the rapid repricing justified?

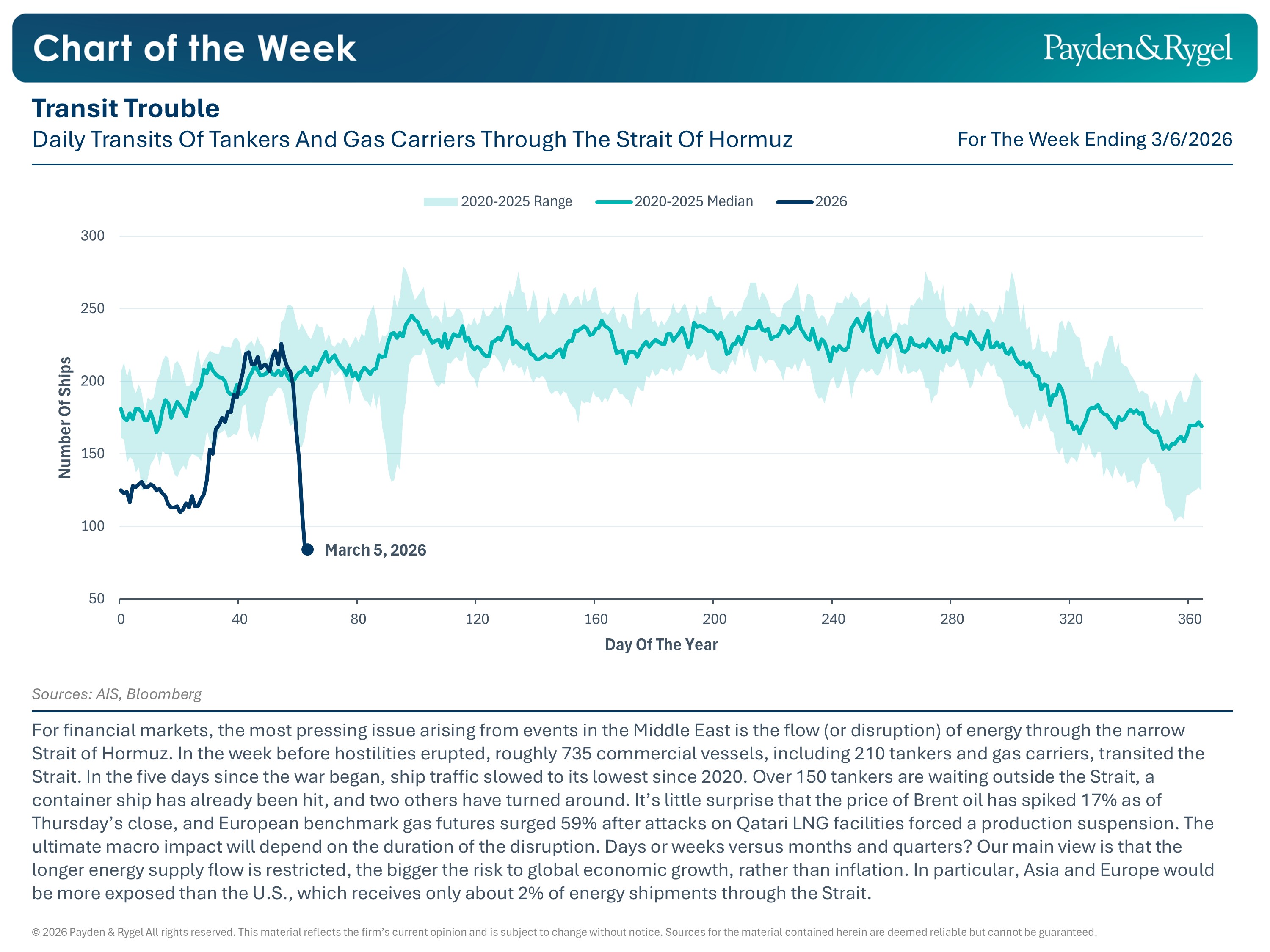

Some readers may quickly reply, "Of course, the world has changed!" Since the eruption of the Middle East conflict at the beginning of March, oil prices have spiked 55%. Ship traffic data suggest that energy-commodity tankers passing through the Strait of Hormuz have slowed from ~200 per week in February to a trickle.

But we’re not so sure the supply shock justifies such a rapid repricing in expectations for four reasons.

First, the standard economic framework suggests that current energy shocks are a “supply shock,” which central banks should “look through.”

A supply shock means prices aren’t surging because global demand is outstripping supply. Instead, due to military action, a large portion of the expected supply has been removed from circulation. The consequent jump in energy prices will filter through the economy, but unless repeated price rises are expected, central banks should “look through” the one-time adjustment. If anything, raising interest rates could further impede supply-side responses, worsening the situation.

Of course, the caveat is that central bankers are “once bitten, twice shy.” The 2022 oil price spike exacerbated an already raging Covid-era inflation problem, and most central banks were too slow to respond. More specifically, as Bank of England outside member Megan Greene has warned, policymakers worry that after “inflation has been above target for the best part of five years, and households and businesses are likely to be more sensitive to upside surprises in inflation given successive negative supply shocks.”1

The inflation expectations response so far varies by country. While short-term inflation expectations have jumped, most gauges of longer-term inflation expectations remain well anchored (see Figures 2 and 3).

{kind=link}

Short Term Market Inflation Expectations By Country, Measured By 1 Year 1 Year Forward CPI Swap

Long Term Market Inflation Expectations Compared To 2010-2019 Average, Measured By 5 Year 5 Year Forward CPI Swap

Second, while we acknowledge the risks posed by the energy shock, global economies are on a completely different footing today than they were in 2022.

Labor markets were much tighter globally when oil prices spiked in 2022, and growth was accelerating (see Figure 4). Today, major economies are collectively shedding jobs (see Figure 5).

Vacancy-To-Unemployed (v/u) Ratio By Country, In January 2022 Versus January 2026

Change In Aggregate Employment Of G7 Nations*

*Data for the U.K. and France are quarterly and assumed constant when the most recent quarter is not available

Specifically, the U.S. lost 330k private sector jobs in the last 12 months after excluding healthcare and education, the most noncyclical sector of the economy. U.S. policymakers seem comforted by continued solid GDP growth, but absent a tech-fueled investment boom, actual growth would have been far more lackluster (see Figure 6).

U.S. Private Sector GDP Growth By Tech And Non-Tech Components*

*Private sector growth measures the sum of Personal Consumption Expenditures and Private Fixed Investment

**Tech = consumer spending and business investment on computer software, hardware, and tech-related infrastructure

In Canada, employment shrank on average in the last three months. In the U.K., an ongoing job slump has pushed the unemployment rate just shy of its Covid-era high (see Figure 7)!

U.K. Unemployment Rate

Also, in the two years leading up to 2022, government transfers to households were massive, including energy subsidies in the EU and record government transfers in the U.S., which contributed to a sudden rise in consumer income. The rise in income meant consumers could absorb rising prices of goods and services and continue spending, contributing to inflation. Today, government transfers are much more muted (see Figure 8).

Average Change In Government Spending In The Two Years Before 2022 And 2026 (Today)*

*Average change in annual (calendar year) government spending

Core inflation, too, averaged 5.7% year-over-year in the U.S., Germany, the UK, and Canada in 2022. Today, both the U.S. and U.K. saw considerable progress in core inflation, while in the euro area and Canada, core inflation has been at target for over a year.

Third, differing exposures to the Middle East oil shock suggest that central banks' reaction functions will also differ.

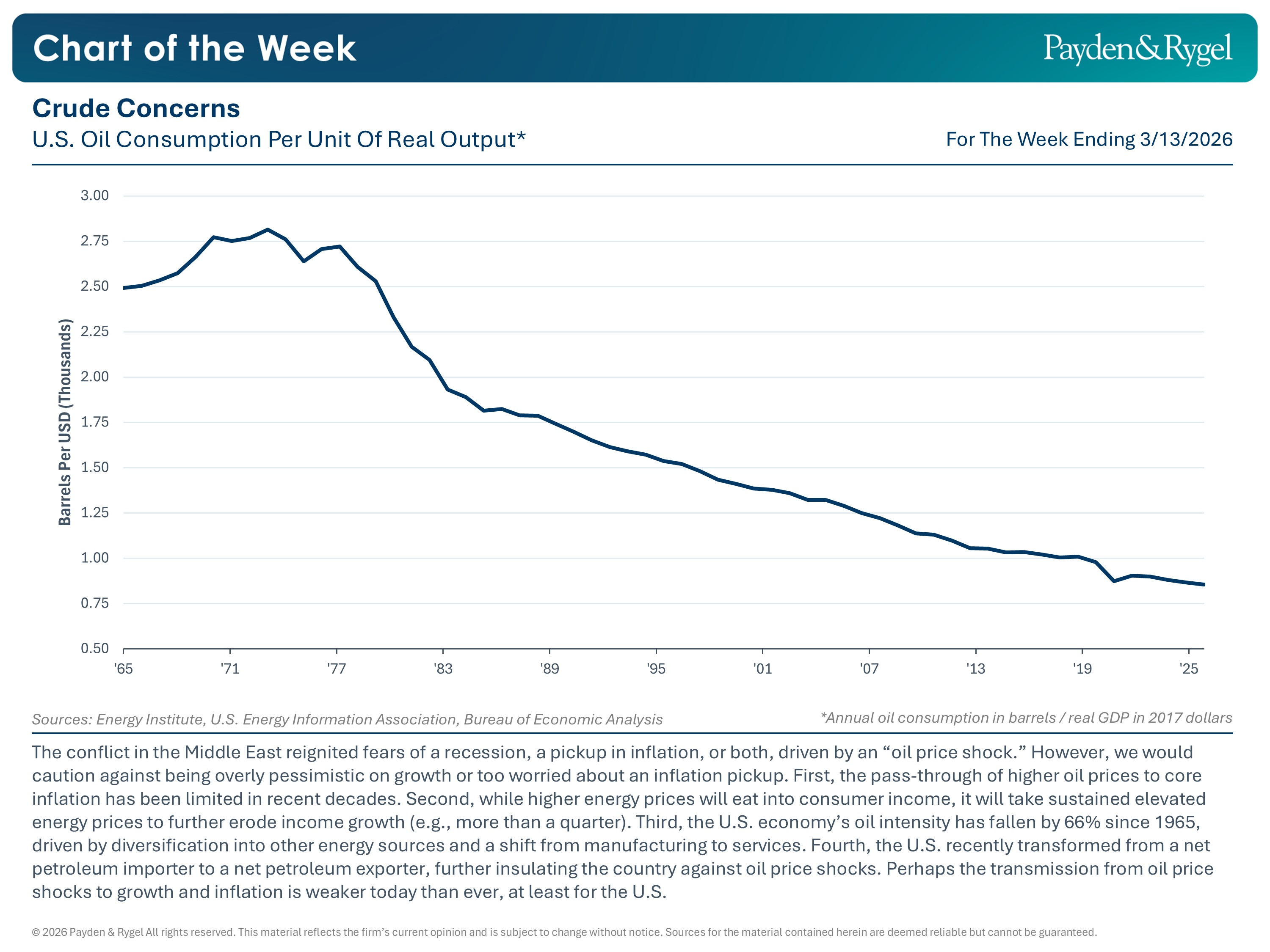

Specifically, the U.S. economy is the most insulated against oil shocks, making the pass-through of higher energy prices to core inflation and domestic growth minimal. Only 7% of U.S. oil imports pass through the Strait of Hormuz, while the U.S. economy’s oil intensity (measured by output per barrel of oil consumed) has decreased nearly 70% since the 1960s. Spending on energy goods and services has also become a smaller share of U.S. consumer disposable income (see Figure 9).

{kind=link}

Energy Goods And Services Spending As A Share Of Nominal Consumer Disposable Income

The Canadian economy is also well insulated, as it is one of the world’s largest crude oil exporters and sits next to the world’s largest liquefied natural gas exporter.2

Meanwhile, exposures are larger in Europe. While the UK imports less than 1% of its natural gas from Qatar, it will be adversely affected by higher energy prices as a net importer of oil, dampening growth in the already weaker UK economy.

Similarly, 60% of the EU’s energy use is imported, of which 67% are petroleum products and 24% are natural gas products. While the Middle East accounts for only 12% of total EU oil imports and 5% of total LNG imports, higher overall oil and LNG prices will weigh much more on growth for a large energy importer like Europe.3

Fourth, central banks’ reaction functions will differ depending on their current policy stance.

The Fed and the Bank of England have both cut rates but have kept monetary policy in restrictive territory due to slow progress in disinflation.

Fed policymakers seem comfortable staying on hold with a relatively stable unemployment rate and even penciled in higher growth expectations in 2026. In turn, the median FOMC member sees only one rate cut in 2026. However, we are still concerned that the labor market is more vulnerable than it was last year, and weaker (or near-zero) job growth may eventually weigh on consumer spending, the backbone of U.S. economic growth.

Similarly, in the UK, policymakers were much more worried about passthrough of core inflation at the March policy meeting. However, if higher energy prices were sustained for more than a quarter, they could dampen growth rather than drive up inflation, leading to more rate cuts than hikes in the U.S. and the U.K.

Meanwhile, the European Central Bank and the Bank of Canada have already kept rates at neutral for over a year, making them more attuned to upside risks to inflation and downside risks to growth.

The bottom line is that a jolt to global bond markets from oil prices could present opportunities for discerning investors with a view that differs from what’s priced in. We don’t think central banks should hike into a supply shock, especially given that global economies in 2026 are in a vastly different shape from 2022.

Always looking for value,

The Payden Economics Team

--

Endnotes

1. Bank of England. (2026, March 19). Monetary policy summary and minutes: March 2026. https://www.bankofengland.co.uk/-/media/boe/files/monetary-policy-summary-and-minutes/2026/monetary-policy-summary-and-minutes-march-2026

2. U.S. Energy Information Administration. (2026, March 18). U.S. natural gas consumption set a monthly and yearly record in 2025. https://www.eia.gov/todayinenergy/detail.php?id=67224

3. Eurostat. (2026, March 18). 47% of EU’s electricity came from renewables in 2025.https://ec.europa.eu/eurostat/web/products-eurostat-news/w/wdn-20260318-1

© 2026 Payden & Rygel. All rights reserved.

This material reflects the firm’s current opinion and is subject to change without notice. Sources for the material contained herein are deemed reliable but cannot be guaranteed. This material is for illustrative purposes only and does not constitute investment advice or an offer to sell or buy any security. Past performance is no guarantee of future results.

This material has been approved by Payden & Rygel Global Limited which is authorised and regulated by the Financial Conduct Authority and by Payden Global SIM S.p.A. which is authorised and regulated by CONSOB.

LOS ANGELES | BOSTON | LONDON | MILAN